Notes to the Financial Statements

For the year ended 30 June 2006

1 First time adoption of Australian equivalents to International Financial Reporting Standards

This is the Public Transport Authority of Western Australia’s (PTA) first published financial statements prepared under Australian equivalents to International Financial Reporting Standards (AIFRS). Accounting Standard AASB 1 ‘First time Adoption of Australian Equivalents to International Financial Reporting Standards’ has been applied in preparing these financial statements. Until 30 June 2005, the financial statements of PTA have been prepared under the previous Australian Generally Accepted Accounting Principles (AGAAP).

The Australian Accounting Standards Board (AASB) adopted the Standards of the International Accounting Standards Board (IASB) for application to reporting periods beginning on or after 1 January 2005 by issuing AIFRS which comprise a Framework for the Preparation and Presentation of Financial Statements, Accounting Standards and the Urgent Issue Group (UIG) Interpretations.

In accordance with the option provided by AASB 1 paragraph 36A and exercised by Treasurer’s Instruction (TI) 1101 ‘Application of Australian Accounting Standards and Other Pronouncements’, financial instrument information prepared under AASB 132 and AASB 139 will apply from 1 July 2005 and consequently comparative information for financial instruments is presented on the previous AGAAP basis. All other comparative information has been prepared under the AIFRS basis.

Early adoption of standards

The PTA cannot early adopt an Australian Accounting Standard or UIG Interpretation unless specifically permitted by TI 1101 ‘Application of Australian Accounting Standards and Other Pronouncements’. This TI requires the early adoption of revised AASB 119 ‘Employee Benefits’ as issued in December 2004, AASB 2004-3 ‘Amendments to Australian Accounting Standards, AASB 2005-3 ‘Amendments to Australian Accounting Standards [AASB 119]’, AASB 2005-4 ‘Amendments to Australian Accounting Standard [AASB 139, AASB 132, AASB 1, AASB 1023 & AASB 1038]’ and AASB 2005-6 ‘Amendments to Australian Accounting Standards [AASB 3]’ to the annual reporting period beginning 1 July 2005. AASB 2005-4 amends AASB 139 ‘Financial Instruments: Recognition and Measurement’ so that the ability to designate financial assets and financial liabilities at fair value is restricted.

Reconciliations explaining the transition to AIFRS as at 1 July 2004 and 30 June 2005 are provided at note 45 ‘Reconciliations explaining the transition to AIFRS’.

2 Summary of significant accounting policies

a) General Statement

The financial statements constitute a general purpose financial report which has been prepared in accordance with the Australian Accounting Standards, the Framework, Statements of Accounting Concepts and other authoritative pronouncements of the Australian Accounting Standards Board as applied by the Treasurer’s Instructions. Several of these are modified by the Treasurer’s Instructions to vary application, disclosure, format and wording.

The Financial Administration and Audit Act and the Treasurer’s Instructions are legislative provisions governing the preparation of financial statements and take precedence over the Accounting Standards, the Framework, Statements of Accounting Concepts and other authoritative pronouncements of the Australian Accounting Standards Board.

Where modification is required and has a material or significant financial effect upon the reported results, details of that modification and the resulting financial effect are disclosed in the notes to the financial statements.

b) Basis of Preparation

The financial statements have been prepared on the accrual basis of accounting using the historical cost convention, modified by the revaluation of land, buildings and infrastructure which have been measured at fair value.

The accounting policies adopted in the preparation of the financial statements have been consistently applied throughout all periods presented unless otherwise stated.

The financial statements are presented in Australian dollars rounded to the nearest thousand dollars ($’000).

The judgements that have been made in the process of applying the PTA’s accounting policies that have the most significant effect on the amounts recognised in the financial statements are disclosed in note 3 ‘Judgements made by management in applying accounting policies’.

The key assumptions made concerning the future, and other key sources of estimation uncertainty at the reporting date that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are disclosed at note 4 ‘Key sources of estimation uncertainty’.

c) Reporting Entity

The Public Transport Authority of Western Australia is the reporting entity and there are no other related or affiliated bodies.

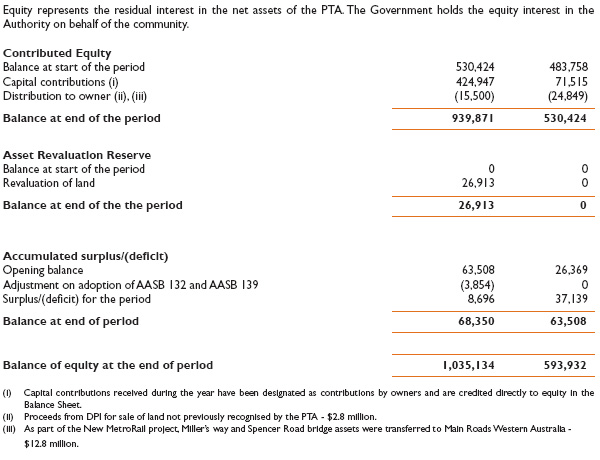

d) Contributed Equity

Under UIG 1038 ‘Contributions by Owners Made to Wholly-Owned Public Sector Entities’ transfers in the nature of equity contributions must be designated by the Government (the owner) as contributions by owners (at the time of, or prior to transfer) before such transfers can be recognised as equity contributions in the financial statements. Capital contributions (appropriations) are designated as contributions by owners by TI 955 ‘Contributions by Owners made to wholly Owned Public Sector Entities’ and have been credited directly to Contributed Equity.

Transfer of net assets to/from other agencies are designated as contributions by owners where the transfers are non-discretionary and non-reciprocal (See note 34 ‘Equity’).

e) Income

Revenue

Revenue is measured at the fair value of consideration received or receivable. Revenue is recognised for the major business activities as follows:

Sale of goods

Revenue is recognised from the sale of goods and disposal of other assets when the significant risks and rewards of ownership control transfer to the purchaser.

Rendering of services

Revenue is recognised on delivery of the service or by reference to the stage of completion except for the following:

i) Cash fares collected by contractors delivering bus services to PTA are accounted for at the time the contract for services invoice is approved for payment.

ii) Fares for MultiRider sales are accounted on a regular basis (at least weekly) when cash is received from sales agents. Unused MultiRider travel entitlements are not recognised in the financial statements.

Interest

Revenue is recognised as the interest accrues.

Service appropriations

Service appropriations are recognised as revenues at nominal value in the period in which the Public Transport Authority of Western Australia (PTA) gains control of the appropriated funds, which is at the time those funds are deposited into the PTA’s bank account or credited to the holding account held at the Department of Treasury and Finance.

Grants, donations, gifts and other non-reciprocal contributions

Revenue is recognised at fair value when PTA obtains control over the assets comprising the contributions. Control is normally obtained upon their receipt.

Other non-reciprocal contributions that are not contributions by owners are recognised at their fair value. Contributions of services are only recognised when a fair value can be reliably determined and the services would be purchased if not donated.

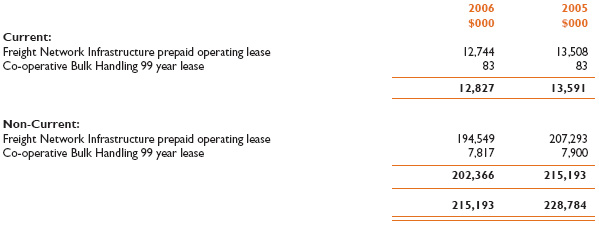

Lease income from operating leases is recognised as income on a straight-line basis over the term of the lease (see Note 13 and 33), with the exception of the 49 years lease of the Freight Network Infrastructure which is based on a net present value annuity schedule.

Gains

Gains may be realised or unrealised and are usually recognised on a net basis. These include gains arising on the disposal of non current assets and some revaluations of non current assets.

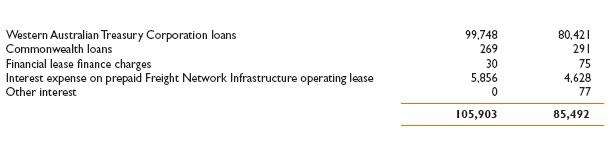

f) Borrowing Costs

All borrowing costs are recognised as expenses in the period in which they are incurred (see Note 3).

g) Infrastructure, Property, Plant and Equipment and Vehicles

Capitalisation/Expensing of assets

Items of property, plant and equipment and infrastructure costing over $5,000 are recognised as assets and the cost of utilising assets is expensed (depreciated) over their useful lives. Items of property, plant and equipment and infrastructure costing less than $5,000 are immediately expensed direct to the Income Statement (other than where they form part of a group of similar items which are significant in total).

Initial recognition and measurement

All items of property, plant and equipment and infrastructure are initially recognised at costs.

For items of property, plant and equipment and infrastructure acquired at no cost or for nominal cost, the cost is their fair value at the date of acquisition.

Subsequent measurement

After recognition as an asset, the revaluation model is used for the measurement of land, buildings and infrastructure and the cost model for all other property, plant and equipment. Land, buildings and infrastructure are carried at fair value less accumulated depreciation on buildings and infrastructure and accumulated impairment losses. All other items of property, plant and equipment are stated at historical cost less accumulated depreciation and accumulated impairment losses.

Where market evidence is available, the fair value of land and buildings is determined on the basis of current market buying values determined by reference to recent market transactions. When buildings are revalued by reference to recent market transactions, the accumulated depreciation is eliminated against the gross carrying amount of the asset and the net amount restated to the revalued amount.

Where market evidence is not available, the fair value of land and buildings is determined on the basis of existing use. This normally applies where buildings are specialised or where land use is restricted. Fair value for existing use assets is determined by reference to the cost of replacing the remaining future economic benefits embodied in the asset, i.e. the depreciated replacement cost. Where the fair value of buildings is dependent on using the depreciated replacement cost, the gross carrying amount and the accumulated depreciation are restated proportionately.

The revaluation of land controlled by the PTA including metropolitan and regional corridor land, not subject to commercial lease has been provided independently by the Department of Land and Information (Valuation Services).

Fair value was determined for all other assets as at 1 July 2003, based on valuation methods to suit specific asset types. Additions since 1 July 2003 have been added to the fair value based on actual cost.

The revaluation of land and buildings which are commercially leased were independently valued based on the capitalised value of current leases.

Rollingstock, permanent way, plant, equipment and vehicles were valued by PTA’s engineering and management professionals based on the written down value of the current cost to replace the asset with a modern equivalent asset capable of delivering the same service potential. The written down value was determined by calculating the unexpired component of each asset’s total useful life.

The Freight Network Infrastructure, subject to a 49 year prepaid lease was valued by an independent expert based on the net present value of the unearned lease income.

Improvements to the Freight Network Infrastructure, funded by the PTA, have been added to the fair value based on actual cost.

Infrastructure, property, plant and equipment is revalued, at least once every five years, to its fair value having regard to its highest and best use.

Construction in progress is recognised at cost.

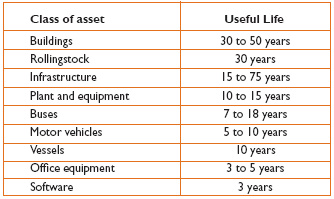

Depreciation

All non-current assets having a limited useful life are systematically depreciated over their estimated useful lives in a manner which reflects the consumption of their future economic benefits.

Land is not depreciated. Depreciation on other assets is calculated on the straight line basis, using rates which are reviewed annually. Expected useful lives for each class of depreciable asset are:

Assets under construction are not depreciated until they are available for use.

h) Intangible Assets

Capitalisation/Expensing of assets

Acquisitions of intangible assets costing over $5,000 are capitalised. The cost of utilising the assets is expensed (amortised) over their useful life. Costs incurred below this threshold are immediately expensed directly to the Income Statement.

All acquired and internally developed intangible assets are initially recognised at cost. For assets acquired at no cost or for nominal cost, the cost is their fair value at the date of acquisition.

The cost model is applied for subsequent measurement requiring the asset to be carried at cost less any accumulated amortisation and accumulated impairment losses.

The carrying value of intangible assets is reviewed for impairment annually when the asset is not yet in use or more frequently when an indicator of impairment arises during the reporting year indicating that the carrying value may not be recoverable.

Amortisation for intangible assets with finite useful lives is calculated for the period of the expected benefit (estimated useful life) on the straight line basis using rates which are reviewed annually. All intangible assets controlled by the PTA have a finite useful life and zero residual value.

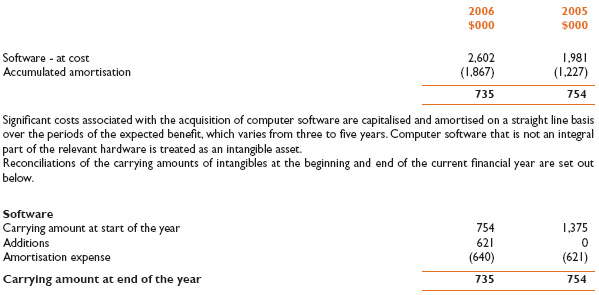

i) Computer software

Software that is an integral part of the related hardware is treated as property, plant and equipment. Software that is not an integral part of the related hardware is treated as an intangible asset and are capitalised and amortised on a straight line basis over the periods of the expected benefit, which varies from 3 to 5 years. Software costing less than $5,000 is expensed in the year of acquisition.

ii) Web site costs

Costs in relation to web sites controlled by the PTA are charged as expenses in the period in which they are incurred.

i) Impairment of Assets

Property, plant and equipment, infrastructure and intangible assets are tested for any indication of impairment at each reporting date. Where there is an indication of impairment, the recoverable amount is estimated. Where the recoverable amount is less than the carrying amount, the asset is written down to the recoverable amount and an impairment loss is recognised. As the PTA is a not for profit entity, unless an asset has been identified as a surplus asset, the recoverable amount is the higher of an asset’s fair value less costs to sell and depreciated replacement cost.

The risk of impairment is generally limited to circumstances where an asset’s depreciation is materially understated or where the replacement cost is falling. Each relevant class of assets is reviewed annually to verify that the accumulated depreciation/amortisation reflects the level of consumption or expiration of asset’s future economic benefits and to evaluate any impairment risk from falling replacement costs.

The recoverable amount of assets identified as surplus assets is the higher of fair value less costs to sell and the present value of future cash flows expected to be derived from the asset. Surplus assets carried at fair value have no risk of material impairment where fair value is determined by reference to market evidence. Where fair value is determined by reference to the depreciated replacement cost, surplus assets are at risk of impairment and the recoverable amount is measured. Surplus assets at cost are tested for indications of impairments at each reporting date.

Refer to note 27 ‘Impairment of Assets’ for the outcome of impairment reviews and testing.

j) Leases

The PTA’s rights and obligations under finance leases, which are leases that effectively transfer to the PTA substantially the entire risks and benefits incident to ownership of the leased items, are initially recognised as assets and liabilities equal in amount to the present value of the minimum lease payments determined at the inception of the lease. The assets are disclosed as plant, equipment and vehicles under lease, and are depreciated to the Income Statement over the period during which PTA is expected to benefit from use of the leased assets. Minimum lease payments are allocated between finance costs and reduction of the lease liability, according to the interest rate implicit in the lease.

Finance lease liabilities are allocated between current and non-current components. The principal component of lease payments due on or before the end of the succeeding year is disclosed as a current liability, and the remainder of the lease liability is disclosed as a non-current liability.

The PTA has entered into a number of operating lease arrangements where the lessor effectively retains the entire risks and benefits incident to ownership of the items held under the operating leases. Equal instalments of the lease payments are charged to the Income Statement over the lease term as this is representative of the pattern of benefits to be derived from the leased assets.

k) Prepaid Lease Revenue

The sale of the Westrail Freight Business on 17 December 2000 included an operating lease of the freight network infrastructure for 49 years between The Western Australian Government Railways Commission (WAGR) – now Public Transport Authority (PTA) and Westnet Rail Pty. The lease rentals were fully prepaid on 17 December 2000, and credited to deferred operating lease revenue. The annual rental from this lease is recognised as revenue, together with an associated interest expense, in accordance with net present value principles.

l) Financial Instruments

The PTA has three categories of financial instruments:

• Loans and receivables (includes cash and cash equivalents, receivables);

• Non-trading financial liabilities (includes finance leases, payables); and

• Financial asset at fair value through profit or loss.Initial recognition and measurement of financial instruments is at fair value which normally equates to the transaction cost or face value. Subsequent measurement is at amortised cost using the effective interest method.

The fair value of short-term receivables and payables is the transaction cost or the face value because there is no interest rate applicable and subsequent measurement is not required as the effect of discounting is not material.

Derivatives are initially recognised at fair value on the date a derivative contract is entered into and are subsequently restated to their fair value at each reporting date. Changes in fair value are recognised through the Income Statement.

m) Cash and Cash Equivalents

For the purpose of the Cash Flow Statement, cash and cash equivalents (and restricted cash and cash equivalents) assets comprise of cash on hand and short-term deposits with original maturities of three months or less that are readily convertible to a known amount of cash and which are subject to insignificant risk of changes in value, and bank overdrafts.

n) Accrued Salaries

Accrued salaries (refer to note 28 ‘Payables’) represent the amount due to staff but unpaid at the end of the financial year, as the end of the last pay period for that financial year does not coincide with the end of the financial year. Accrued salaries are settled within a few days of the financial year end. The PTA considers the carrying amount approximates net fair value.

o) Amounts Receivable for Services (Holding Account)

The PTA receives funding on an accrual basis that recognises the full annual cash and non-cash cost of services. The appropriations are paid partly in cash and partly as an asset (Holding Account receivable) that is accessible on the emergence of the cash funding requirement to cover items such as leave entitlements and asset replacement. See also note 19 ‘Income from State Government’ and note 23 ‘Amounts receivable for services’.

p) Inventories

Inventories are measured at the lower of cost and net realisable value. Costs are assigned by the method most appropriate to each particular class of inventory. Inventory recorded using the inventory control system is valued at the weighted average cost whereas the balance is valued on a first in first out basis.

Inventories not held for resale are valued at cost unless they are no longer required, in which case they are valued at net realisable value.

See note 21 ‘Inventories’.

q) Receivables

Receivables are recognised and carried at original invoice amount less any provision for uncollectible amounts (impairment). The collectability of receivables is reviewed on an ongoing basis. Debts which are known to be uncollectible are written off. A provision for doubtful debts is raised when there is objective evidence that the PTA will not be able to collect the debts.

The carrying value is equivalent to fair value as it is due for settlement within 30 days.

See note 2(l) ‘Financial Instruments’ and note 22 ‘Receivables’.

r) Payables

Payables, including accruals not yet billed, are recognised when the PTA becomes obliged to make future payments as a result of a purchase of assets or services.

The carrying value is equivalent to fair value as it is due for settlement within 30 days.

See note 2(l) ‘Financial Instruments’ and note 28 ‘Payables’.

s) Borrowings

All loans are initially recorded at cost, being the fair value of the net proceeds received. Subsequent measurement is at amortised cost using the effective interest rate method.

See note 2(l) ‘Financial Instruments’ and note 29 ‘Borrowings’.

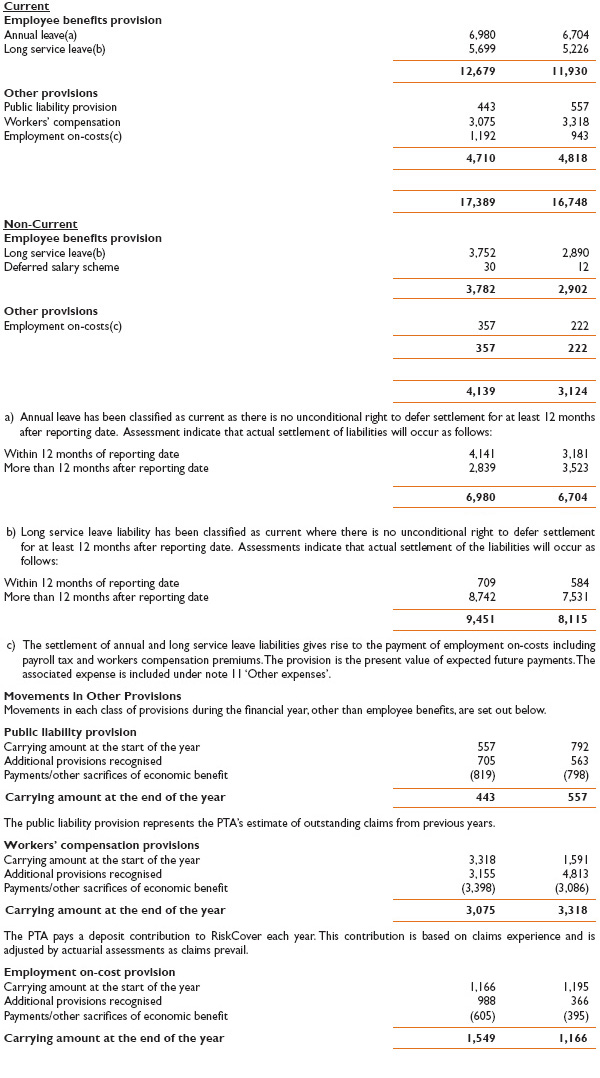

t) Provisions

Provisions are liabilities of uncertain timing and amount and are recognised where there is a present legal, equitable or constructive obligation as a result of a past event and when the outflow of economic benefits is probable and can be measured reliably. Provisions are reviewed at each balance date. See note 30 ‘Provisions’

(i) Provisions - Employee Benefits

Annual Leave and Long Service Leave

The liability for annual and long service leave expected to be settled within 12 months after the end of the reporting date is recognised and measured at the undiscounted amounts expected to be paid when the liabilities are settled. Annual and long service leave expected to be settled more than 12 months after the end of the reporting date is measured at the present value of amounts expected to be paid when the liabilities are settled. Leave liabilities are in respect of services provided by employees up to the reporting date.

When assessing expected future payments consideration is given to expected future wage and salary levels including non salary components such as employer superannuation contributions. In addition, the long service leave liability also considers the experience of employee departures and periods of service.

The expected future payments are discounted using market yields at the reporting date on national government bonds with terms to maturity that match, as closely as possible, to the estimated future cash outflows.

All annual and unconditional long service leave provisions are classified as current liabilities as the PTA does not have an unconditional right to defer settlement of the liability for at least 12 months after the reporting date.

Sick Leave

Liabilities for sick leave are recognised when it is probable that sick leave paid in the future will be greater than the entitlement that will accrue in the future.

Past history indicates that on average, sick leave taken each reporting period is less than the entitlement accrued. This is expected to continue in future periods. Accordingly, it is unlikely that existing accumulated entitlements will be used by employees and no liability for unused sick leave entitlements is recognised. As sick leave is non-vesting, an expense is recognised in the income statement for this leave as it is taken.

Superannuation

The Government Employees Superannuation Board (GESB) administers the following superannuation schemes.

Staff may contribute to the Pension Scheme, a defined benefit pension scheme now closed to new members, or to the Gold State Superannuation (GSS) Scheme, a defined benefit lump sum scheme now also closed to new members. The PTA has no liabilities under the Pension or the GSS Schemes.The liabilities for the unfunded Pension Scheme and the unfunded GSS Scheme transfer benefits due to members who transferred from the Pension Scheme, are assumed by the Treasurer. All other GSS Scheme obligations are funded by concurrent contributions made by the PTA to the GESB. The concurrently funded part of the GSS Scheme is a defined contribution scheme as these contributions extinguish all liabilities in respect of the concurrently funded GSS Scheme obligations.

Employees who are not members of either the Pension or the GSS Schemes become non-contributory members of the West State Superannuation (WSS) Scheme. The PTA makes concurrent contributions to GESB on behalf of employees in compliance with the Commonwealth Government’s Superannuation Guarantee (Administration) Act 1992. The WSS Scheme is a defined contribution scheme as these contributions extinguish all liabilities in respect of the WSS Scheme. See also note 2(u) ‘Superannuation expense’.

The GESB makes all benefit payments in respect of the Pension and GSS schemes and is recouped by the Treasurer for the employer’s share.

(ii) Provisions - Other

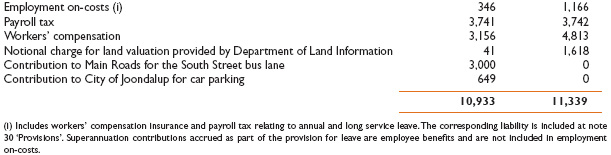

Employment On-Costs

Employment on-costs, including payroll tax and workers’ compensation insurance, are not employee benefits and are recognised as separate liabilities and expenses when the employment to which they relate has occurred.

Employment on-costs are not included as part of the PTA’s ‘Employee benefits expense’ and the related liability is included in Employment on-costs provision (see notes 5 and 30).

u) Superannuation Expense

The following elements are included in calculating the superannuation expense in the Income Statement:

i) Defined benefit plans – change in the unfunded employers’ liability (i.e. current service cost and actuarial gains and losses) assumed by the Treasurer in respect of current employees who are members of the Pension Scheme and current employees who accrued a benefit on transfer from that Scheme to the Gold State Superannuation Scheme (GSS); and

ii) Defined contribution plans – employer contributions paid to the GSS and the West State Superannuation Scheme (WSS).

v) Resources Received Free of Charge or for Nominal Cost

Resources received free of charge or for nominal cost which can be reliably measured are recognised as revenues and as assets or expenses as appropriate at fair value.

w) Comparative Figures

Comparative figures have been restated on the AIFRS basis except for financial instruments which have been prepared under the previous AGAAP Australian Accounting Standard AAS 33. The transition date to AIFRS for financial instruments is 1 July 2005 in accordance with the exemption allowed under AASB 1, paragraph 36A and Treasurer’s Instruction 1101.

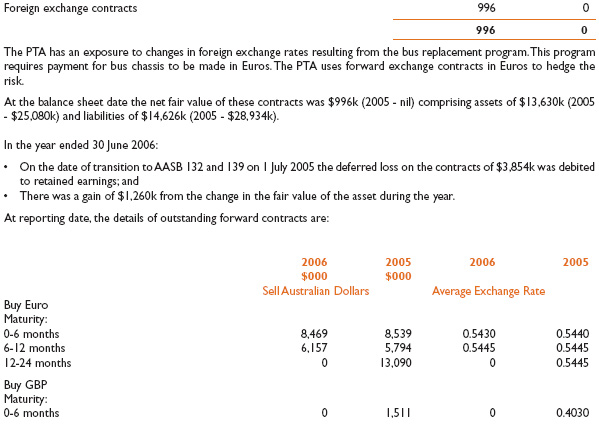

x) Derivatives

The Public Transport Authority has exercised the exemption available under AASB 1.36A and as per the Treasurer’s Instruction 1101 to apply AASB 132 and AASB 139 from 1 July 2005. The PTA has applied previous AGAAP for the comparative period ending 30 June 2005 (see note 2w) for comparative information.

Forward foreign exchange contracts from 1 July 2004 and 30 June 2005.

The PTA has applied previous AGAAP for the comparative period ending 30 June 2005.

Under the previous AGAAP gains or losses from entering into a contract intended to hedge the purchase of goods together with the subsequent gains or losses resulting from the restatement of those contracts by reference to movements in spot exchange rates were deferred in the balance sheet from the inception of the hedging transaction up to the date of the purchase and included in the subsequent purchase price of the assets.

Adjustments on transition date: 1 July 2005

At the date of transition, 1 July 2005, in line with AASB 132 and AASB 139 the foreign exchange contracts were measured on the fair value basis. The changes in the fair value were taken to retained earnings.

For future information concerning adjustments on transition date reference should be made to: Note 32 ‘Derivatives’, Note 39 ‘Financial Instruments’ and Note 34 ‘Equity’.

From 1 July 2005

The foreign exchange contracts are initially recognised at fair value on the date the contract is entered into and are subsequently restated to their fair value at each reporting date. Changes in the fair value of the contracts are recognised in the income statement and are included in the income or other expenses.

At balance date the amount receivable and payable under the foreign exchange contracts are disclosed on a net basis representing the future cash flow required to settle the contracts.

y) Foreign Currency Translation

Transactions denominated in a foreign currency are translated at the rates in existence at the dates of the transactions. Foreign currency receivables and payables at reporting date are translated at exchange rates current at reporting date. Exchange gains and losses are brought to account in determining the result for the year.

z) Future impact of Australian Accounting Standards not yet operative

The PTA cannot early adopt an Australian Accounting Standard or UIG Interpretation unless specifically permitted by TI 1101 ‘Application of Australian Accounting Standards and Other Pronouncements’. As referred to in Note 1, TI 1101 has only mandated the early adoption of revised AASB 119, AASB 2004-3, AASB 2005-3, AASB 2005-4 and AASB 2005-6.

Consequently, the PTA has not applied the following Australian Accounting Standards and UIG Interpretations that have been issued but are not yet effective. These will be applied from their application date:a) AASB 7 ‘Financial Instruments: Disclosures’ (including consequential amendments in AASB 2005-10 ‘Amendments to Australian Accounting Standards [AASB 132, AASB 101, AASB 114, AASB 117, AASB 133, AASB 139, AASB 1, AASB 4, AASB 1023 & AASB 1038]’).

This Standard requires new disclosures in relation to financial instruments. The Standard is required to be applied to annual reporting periods beginning on or after 1 January 2007. The Standard is considered to result in increased disclosures of an entity’s risks, enhanced disclosure about components of a financial position and performance, and changes to the way of presenting financial statements, but otherwise there is no financial impact.

b) AASB 2005-9 ‘Amendments to Australian Accounting Standards [AASB 4, AASB 1023, AASB 139 & AASB 132]’ (Financial guarantee contracts).

The amendment deals with the treatment of financial guarantee contracts, credit “insurance contracts”, letters of credit or credit derivative default contracts as either an “insurance contract” under AASB 4 “Insurance Contracts” or as a “financial guarantee contract” under AASB 139 ‘Financial Instruments: Recognition and Measurement’.

The PTA does not undertake these types of transactions resulting in no financial impact when the Standard is first applied.

The Standard is required to be applied to annual reporting periods beginning on or after 1 January 2006.

c) UIG Interpretation 4 ‘Determining whether an Arrangement Contains a Lease’.

This Interpretation deals with arrangements that comprise a transaction or a series of linked transactions that may not involve a legal form of a lease but by their nature are deemed to be leases for the purposes of applying AASB 117 ‘Leases’.At reporting date, the PTA has not entered into any arrangements as specified in the Interpretation resulting in no impact when the Interpretation is first applied. The Interpretation is required to be applied to annual reporting periods beginning on or after 1 January 2006.

The following amendments are not applicable to the PTA as they will have no impact:

i) 2005-1 AASB 139: (Cash flow hedge accounting of forecast intragroup transactions).

ii) 2005-5 ‘Amendments to Australian Accounting Standards [AASB 1 & AASB 139]’.

iii) 2006-1 AASB 121 (Net investment in foreign operations).

iv) UIG 5 ‘Rights to Interests arising from Decommissioning, Restoration and Environmental Rehabilitation Funds’.

v) UIG 6 ‘Liabilities arising from Participating in a Specific Market – Waste Electrical and Electronic Equipment’.

vi) UIG 7 ‘Applying the Restatement Approach under AASB 129 Financial Reporting in Hyperinflationary Economies’.

vii) UIG 8 ‘Scope of AASB 2’.

viii) UIG 9 ‘Reassessment of Embedded Derivatives’.

3 Judgement made by management in applying accounting policies

The judgements that have been made in the process of applying accounting policies that have the most significant effect on the amounts recognised in the financial statements include:

- The PTA has decided to expense all borrowing costs associated with the construction of major projects such as New MetroRail as allowed by the alternative accounting treatment under AASB 123 ‘Borrowing Costs’.

4 Key sources of estimation uncertainty

The key assumptions made concerning the future, and other key sources of estimation uncertainty at the reporting date that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year include:

Discount rates used in estimating provisions

The PTA is using market yields on national government bonds with terms to maturity that match, as closely as possible, to the estimated future cash outflows to discount the estimated value of the provisions for annual and long service leave. Fluctuations in the government bond yields may impact the provision for annual and long service leave.

Estimating useful life of key assets

The useful lives are estimated having regard to such factors as asset maintenance, rate of technical and commercial obsolescence, asset usage. The useful lives of key assets are reviewed annually.

The useful life of the Freight Network Infrastructure is based on the term of the lease.

7 Depreciation and amortisation expense

9 Grants and subsidies expense

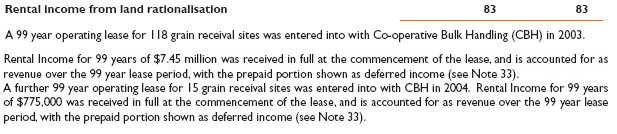

13 Land rationalisation lease revenue

15 Grants and subsidies revenue

18 Net gain/(loss) on disposal of non-current assets

19 Income from State Government

20 Restricted cash and cash equivalents

23 Amounts receivable for services

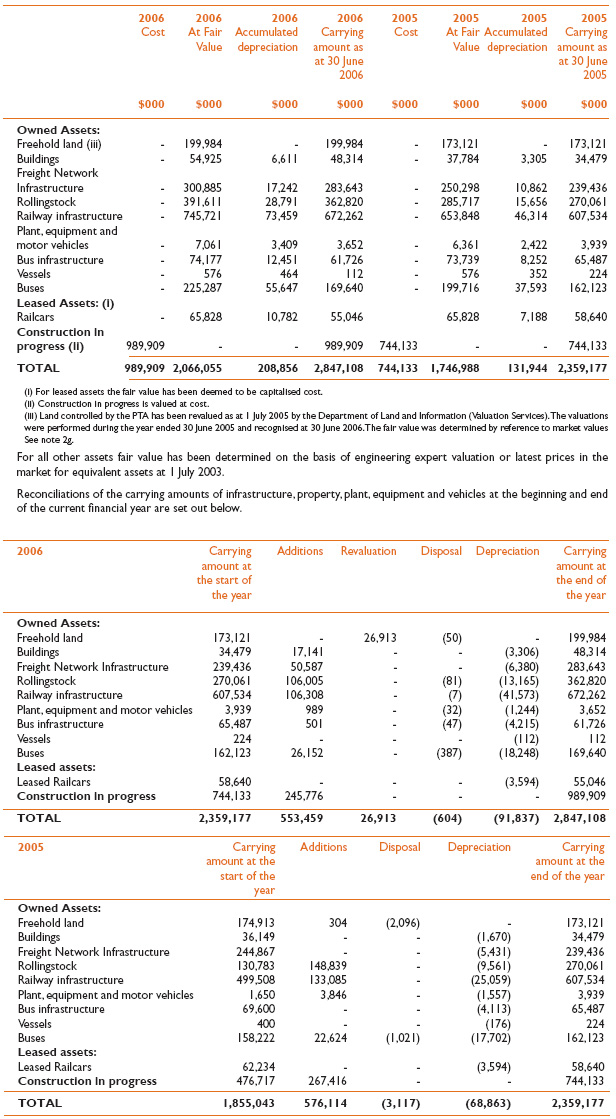

25 Infrastructure, property, plant, equipment and vehicles

33 Deferred income – operating leases

35 Notes to the Cash Flow Statement

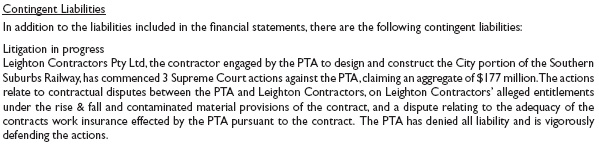

37 Contingent liabilities and contingent assets

38 Remuneration of members of the Accountable Authority and senior officers

40 Supplementary financial information

41 Events occurring after the balance sheet date

![]()

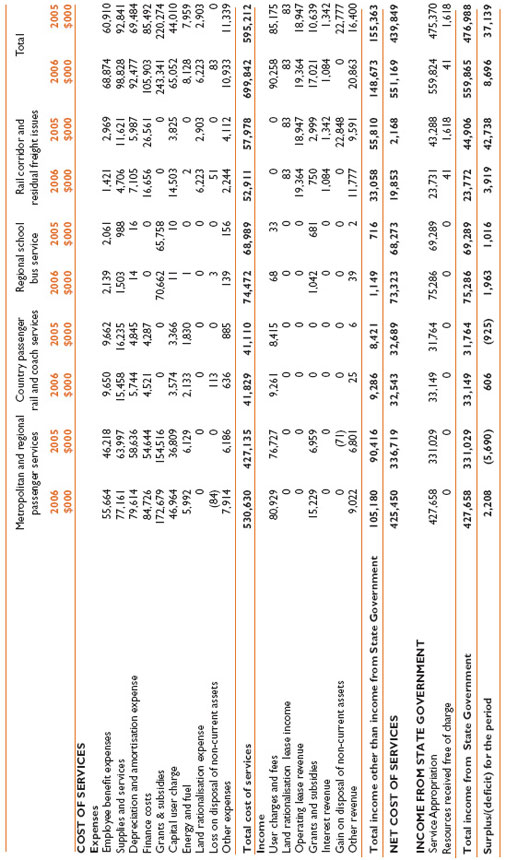

43 Schedule of income and expenses by service

(click here for web friendly version of this page)

45 Reconciliations explaining the transition to Australian equivalents to International Financial Reporting Standards (AIFRS)

Notes to reconciliations

Note 45.1 Intangible assets (AASB 138)

AASB 138 requires that software not integral to the operation of a computer must be disclosed as intangible assets. Intangible assets must be disclosed on the balance sheet. All software has previously been classified as property, plant and equipment (office equipment). The following adjustments have been made:

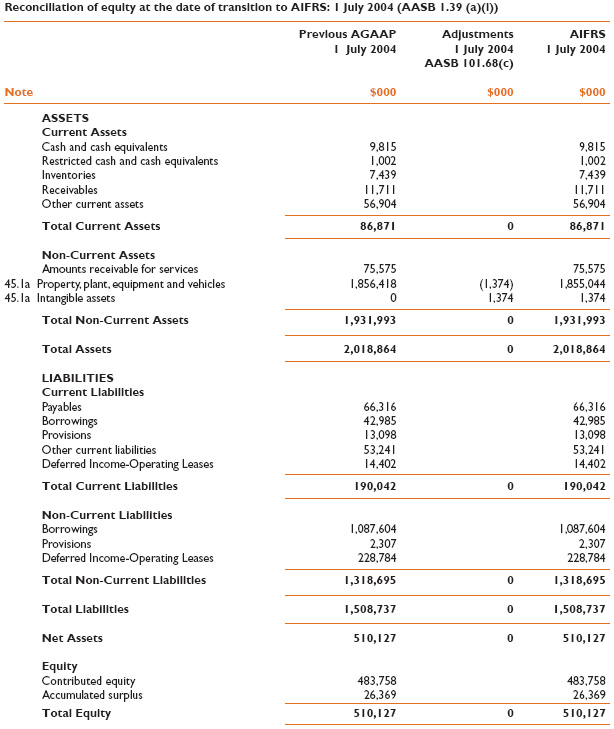

45.1a Adjustments to opening Balance Sheet (1 July 2004)

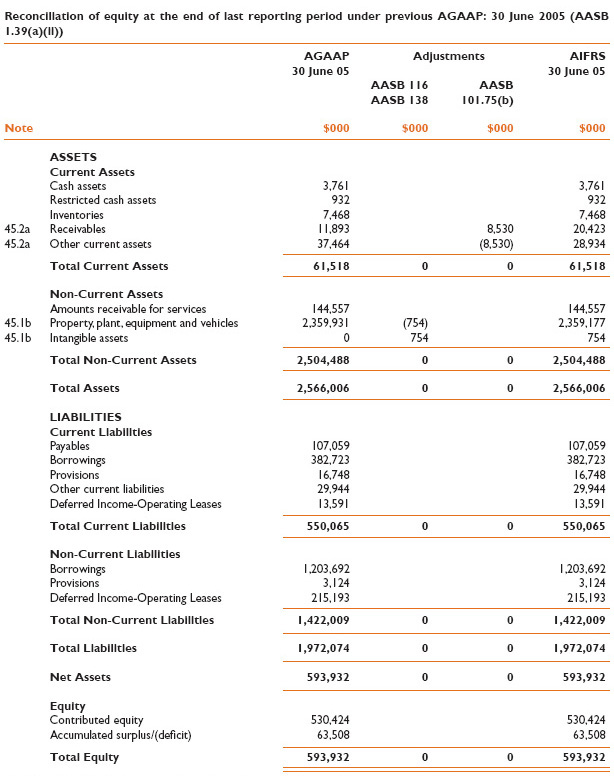

The PTA has transferred $1,374k in software from property, plant and equipment to intangible assets.45.1b Adjustments to 30 June 2005 Balance Sheet

The PTA has transferred $754k in software from property, plant and equipment to intangible assets. This represents the opening balance sheet adjustment of $1,374k less $621k depreciation for the year.

Note 45.2 Receivable (AASB101)

AASB 101 requires receivables be disaggregated into amounts receivable from trade customers, prepayments and other amounts.

45.2a Adjustments to 30 June 2005 Balance Sheet

Prepayments and cash advances on New MetroRail project have been reclassified from ‘Other assets’ to ‘Receivables’ ($8,530k).

Note 45.3 Employee benefits (AASB 119 and AASB 101)

Employment on-costs are not included in employee benefits under AGAAP or AIFRS. However, under AGAAP employee benefits and on-costs are disclosed together on the face of the Income Statement as employee costs. Under AIFRS employee benefits will be the equivalent item disclosed on the face. On-costs are transferred to other expenses.

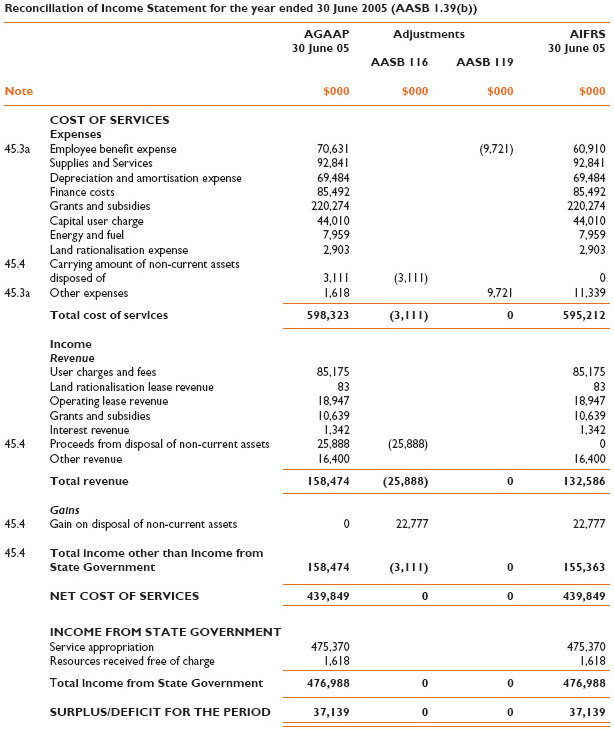

45.3a Adjustments to the Income Statement for the period ended 30 June 2005

Employment on-costs expense has been reclassified from employee benefits expense to other expense ($9,721k).

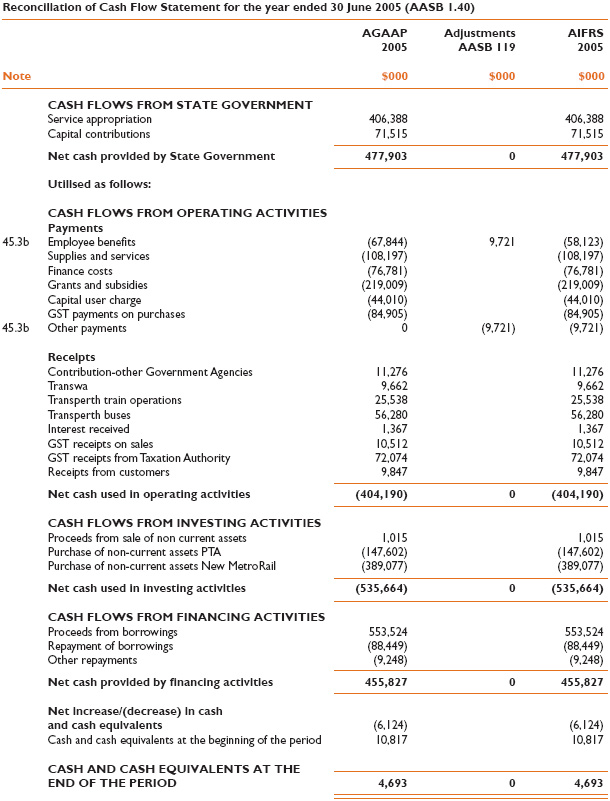

45.3b Adjustments to the Cash Flow Statement for the period ended 30 June 2005

Employment on-costs payments have been reclassified from employee benefit payments to other payments ($9,721k).

Note 45.4 Net gain on disposal of non-current assets (AASB 116)

Under AGAAP the disposal of non-current assets is disclosed on the gross basis. That is, the proceeds of disposal are revenue and the carrying amounts of assets disposed of are expense. The disposal of non-current assets is disclosed on the net basis (gains or losses) under AIFRS.

Adjustments to the Income Statement for the period ended 30 June 2006

The carrying amounts of assets disposed of were previously recognised as expense. This has been derecognised ($3,111k).

The proceeds of disposal of non-current assets were previously recognised as income. This has been derecognised ($25,888k).

A gain on the disposal of non-current assets of $22,777k has been recognised as income.

>> Go to top